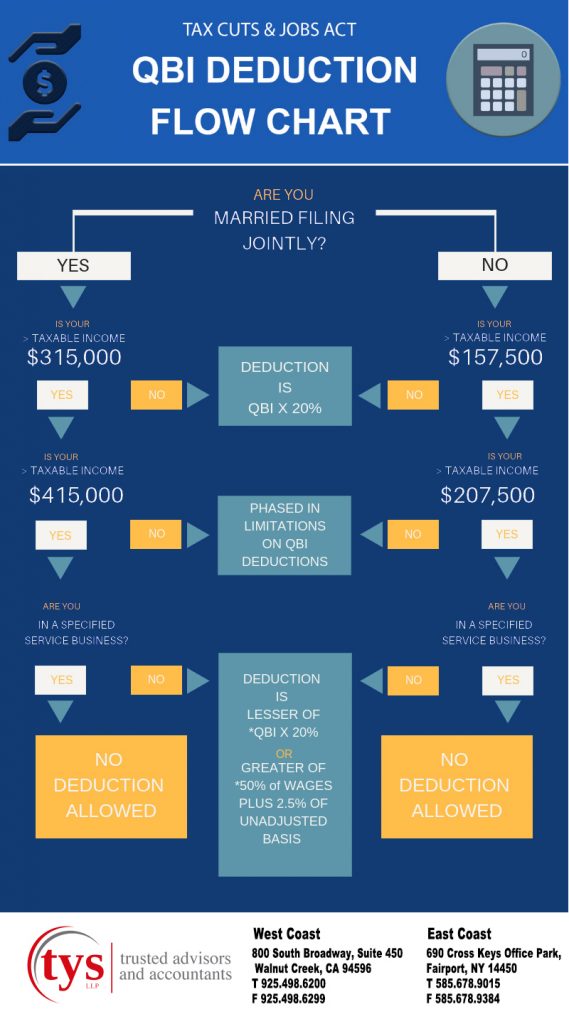

QBI Deduction explained

The 21st century has seen a great many changes on how we work, live and play. We pretty much have abandoned the idea of working at one company for our whole careers. In fact of the freelancer or a sole proprietor part of the economy has blossomed. The Brookings Institute calls this trend the “Gig” economy and it is growing. If you are one of those in the “gig” economy you might have heard of the new 199A that is part of the Tax Cuts and Jobs Act (TCJA). 199A provides taxpayers a deduction of up to 20% of qualified business income (QBI) earned from a business operated as a sole proprietorship, a partnership, S corporation, trust, or estate. So do you qualify, well maybe. Are you a sole proprietor?

According to the U.S. Small Business Administration a sole proprietor –

“is the simplest and most common structure chosen to start a business. It is an unincorporated business owned and run by one individual with no distinction between the business and you, the owner. You are entitled to all profits and are responsible for all your business’s debts, losses and liabilities.”. https://www.sba.gov/content/sole-proprietorship

Don’t get too excited just yet, you might benefit from the 199A under the QBI but there are still questions raised about who exactly is entitled to the benefit. There are various limitations and interpretations, so now more than at any other recent tax season, you should talk to a tax professional. The tax experts at TYS would be happy to speak with you and help guide you through the labyrinth of the new tax laws.

You have heard some of the news reports about taxpayers expecting a tax return, who end up having to pay Uncle Sam instead. We hope that doesn’t happen to you. If you are part of the gig economy you may want to look at what it cost you to do business in the form of expenses. You might be leaving money on the table and no one wants that to happen.